(This is the 7th article of this seminar series composed of 11 articles)

(Part 7) Profit Split Method

1. Profit Split Method

The Profit Split Method can be divided into three sub-methods: the Comparable Profit Split Method, the Contribution Profit Split Method, and the Residual Profit Split Method. The Profit Split Method would be effective when there are no comparable companies available, as already explained in Part 4 of this series. While we have not found any practical examples using the Comparable Profit Split Method, which relies on comparable uncontrolled transactions, the Contribution Profit Split Method and the Residual Profit Split Method in practice are more often employed. The former is appropriate when the controlled transactions are highly integrated, and the latter is used when both parties to the controlled transactions perform unique functions and utilize intangible assets of their own.

The most important point in the Profit Split Method is how to assess the factors used to justify the split (i.e., factors concerning the two parties, which must be sufficient to estimate the extent of the parties’ contributions to the generation of profits). For example, research and development (R&D) expenses can be used as a splitting factor when it is known that the intangible assets of one party have contributed to the generation of profits. Advertising expenses can be used when one party’s advertising activities have contributed to the generation of profits. However, it is fairly difficult to analyze and explain the relevancy and extent of the parties’ contributions and the resulting split.

2.Comparable Profit Split Method

The Comparable Profit Split Method determines the arm’s-length price by allocating the profit gained in controlled transactions to either the company or its affiliate through the application of a ratio equivalent to the profit split ratio found in uncontrolled transactions conducted under similar circumstances.

3.Contribution Profit Split Method

The Contribution Profit Split Method determines the arm’s-length price by allocating the total amount of operating profit (profit to be split) earned by the two parties in controlled transactions to either the company or its affiliate in proportion to the factors that contributed to each party’s ability to generate the profit (splitting factors). The applicability of this method increases in cases where the controlled transactions are highly integrated, since it does not require the presence of comparable unrelated companies.

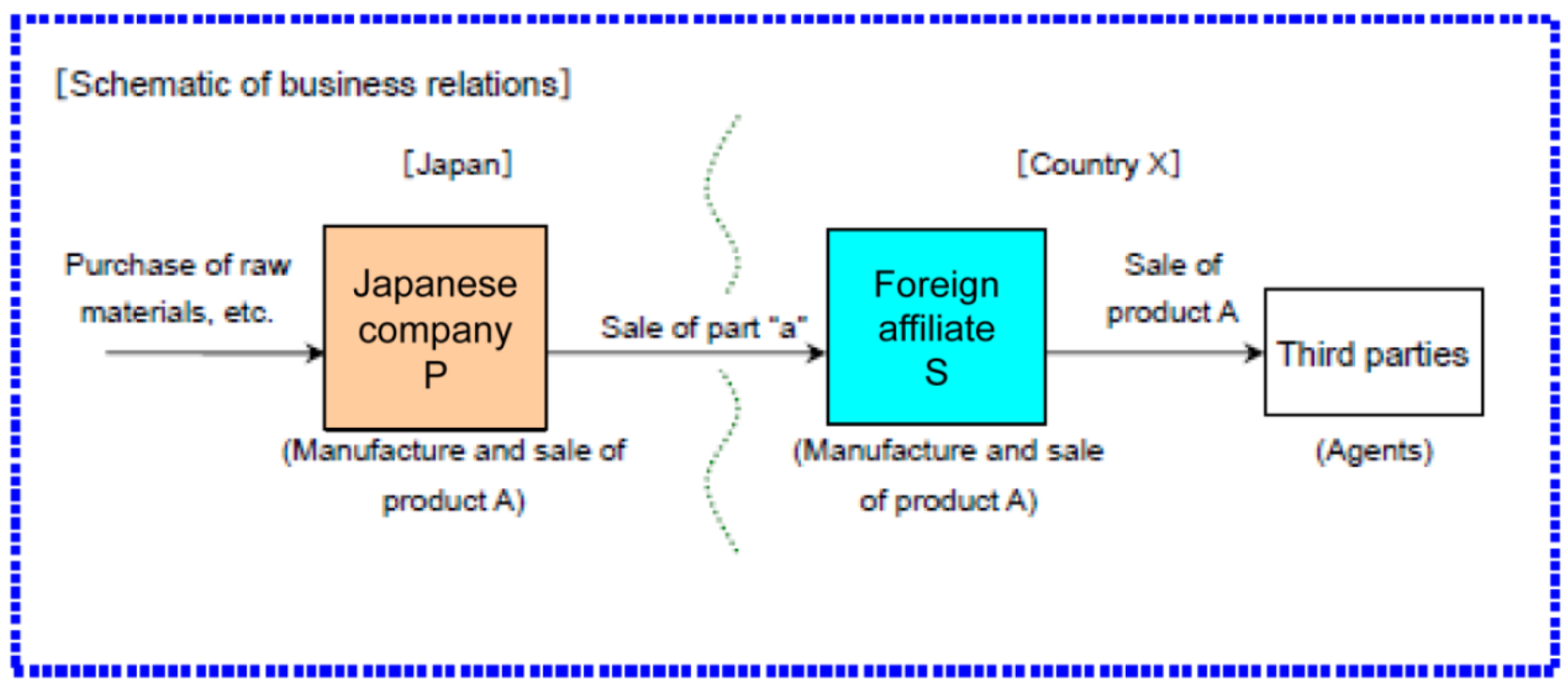

Case 7, “Use of the Contribution Profit Split Method,” in the Reference Case Studies explains the transactions described in the chart below. In addition to company S, there are two more companies (manufacturing subsidiaries whose parent companies reside outside county X). All three companies manufacture and sell products similar to product A in terms of product performance and price in country X, and all three share the market equally. Only one company manufactures and sells a product similar to company P’s product A in Japan, and that company conducts controlled transactions only. In such a case, it is considered appropriate to calculate the arm’s-length price for the controlled transactions through the Contribution Profit Split Method.

[Source:“Case 7” of “Reference Case Studies on Application of Transfer Pricing Taxation,” National Tax Agency]

Regarding the factors for splitting profits, the amount of personnel expenses, invested capital, etc., are factors appropriate for estimating the extent of the parties’ contributions to the generation of the profit to be split. It is reasonable to employ personnel expenses to reflect the functions or depreciation expenses when functions that are routinely performed, such as in manufacturing or sales, contribute to the generation of the profits.

4.Residual Profit Split Method

The Residual Profit Split Method allocates the combined profits (profits to be split) in the controlled transactions by following the two steps described below when it is recognized that both parties in the controlled transactions have made unique and valuable contributions by performing their own original functions. The arm’s-length price is calculated by:

- calculating and allocating the profits (basic profits) generated in the transactions on the assumption that the parties to the controlled transactions do not perform any unique functions, and then

- allocating the residual amount left after deducting the basic profits to the parties in proportion to the unique and valuable contributions of each party.

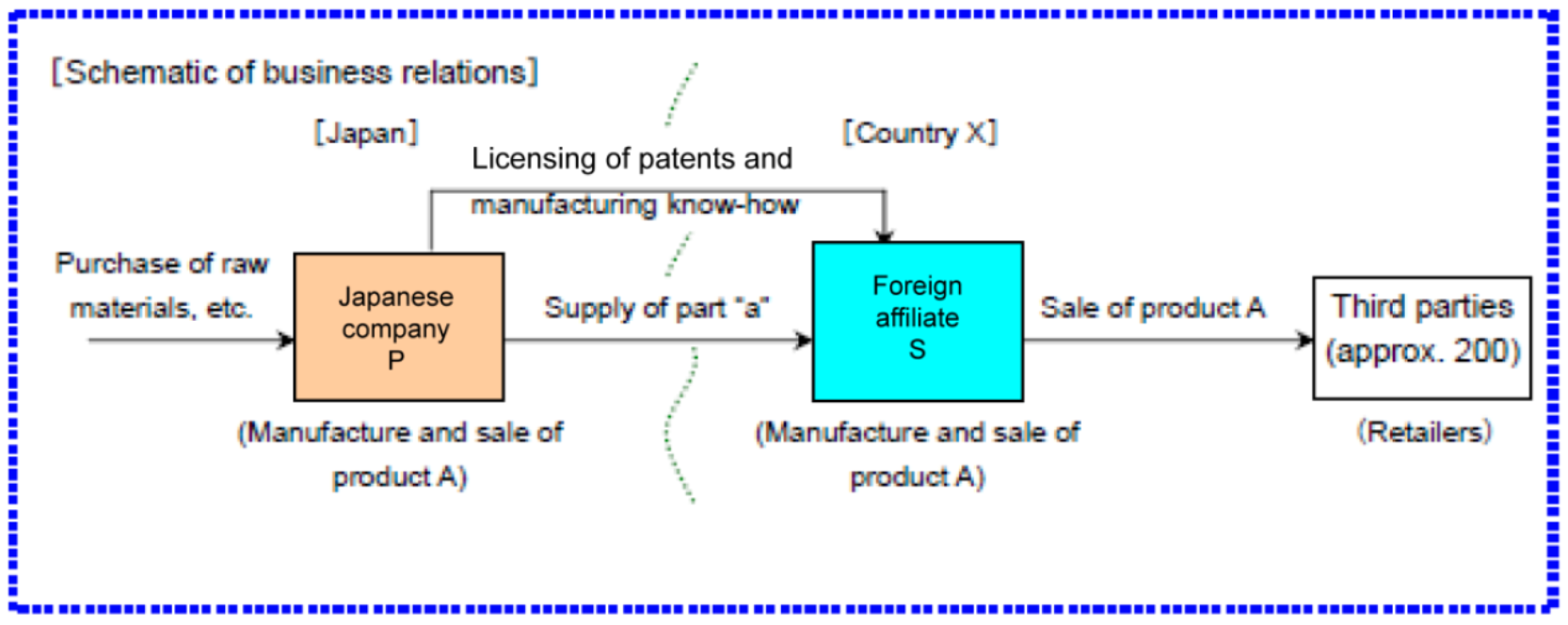

Case 8, “Use of the Residual Profit Split Method” in the Reference Case Studies explains the transactions described in the chart below. This example shows that company S does not have an R&D division and simply manufactures product A based on the unique technology and techniques provided by company P. On the other hand, company S has numerous sales representatives and engages in its own advertising and sales promotion activities targeting retailers and end-use consumers. Product A has achieved a certain market share in country X owing to its unique technical performance, its high consumer awareness, and its highly developed retailer network built through advertising and sales promotion. The product is mostly sold at a stable price. In such a case, it is considered appropriate to calculate the arm’s-length price by employing the Residual Profit Split Method.

[Source: “Case 8” of “Reference Case Studies on Application of Transfer Pricing Taxation,” National Tax Agency]

In transfer pricing taxation, the R&D activities of company P and the advertising and sales promotion activities of company S are each considered to have originality and uniqueness and thus are distinctive intangible assets that place the product in a relatively superior position in economic competition with other products. In this example, it is appropriate to employ the Residual Profit Split Method to calculate the arm’s-length price, as both the company and its foreign affiliate use intangible assets to make original and valuable contributions in generating profits.

(The next article in this “Transfer Pricing Seminar Series for Medium-sized Corporations in Japan” will be published next month.)

For further inquiries, please contact us at Japan@HLS-Global.jp.

Transfer Pricing Seminar Series Articles:

- (Part 1) Working Seminar for Medium-sized Corporations Unfamiliar with Transfer Pricing

- (Part 2) Overview of Transfer Pricing Taxation

- (Part 3) Transfer Pricing Examinations, Advance Pricing Agreements, and Documentation

- (Part 4) Transfer Pricing Methods to determine the Arm’s Length Price

- (Part 5) Traditional Transaction Methods

- (Part 6) Transactional Net Margin Method: TNMM

- (Part 7) Profit Split Method

- (Part 8) Considerations to prepare the Local File

- (Part 9) Considerations When Preparing Local Files

- (Part 10) Selection of the comparable companies and calculation of the profitability range

- (Part 11) Transfer Pricing Policy and Transfer Pricing Documentations